With higher-than-expected tariffs India’s GDP outlook is at risk. The damage could be to the tune of 30-50 bps.

This could well mean our FY 26 GDP growth just a tad above 6%.

As such private capex was slow and with increasing uncertainty it's contribution to growth can continue to be lower. Hence, we believe there is a downside risk to Nifty EPS growth projections (1200) for FY 26.

The growth can be stock specific and not secular. Therefore, clearly, it's better to invest in actively managed equity funds systematically.

With all the negative news around the real savior could be RBI.

In a world of recession risks and supply chain disruptions, a strong recovery in India’s domestic demand has become even more critical.

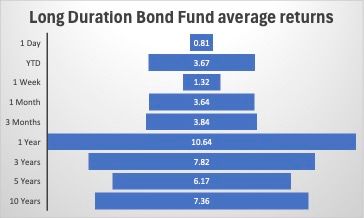

Hence, RBI is expected to frontload its rate cuts now. There is a good probability of aggressive rate cuts and therefore we suggest you allocate more investments to Long Duration debt funds that invest in government securities.

The recent returns are high due to fall in interest rates and the same could be possible going forward.

Feel free to call us if you have any queries.