After remaining relatively cautious on Indian equities for almost a year, we have finally started increasing allocations toward Indian equity markets.

The reason is straightforward:

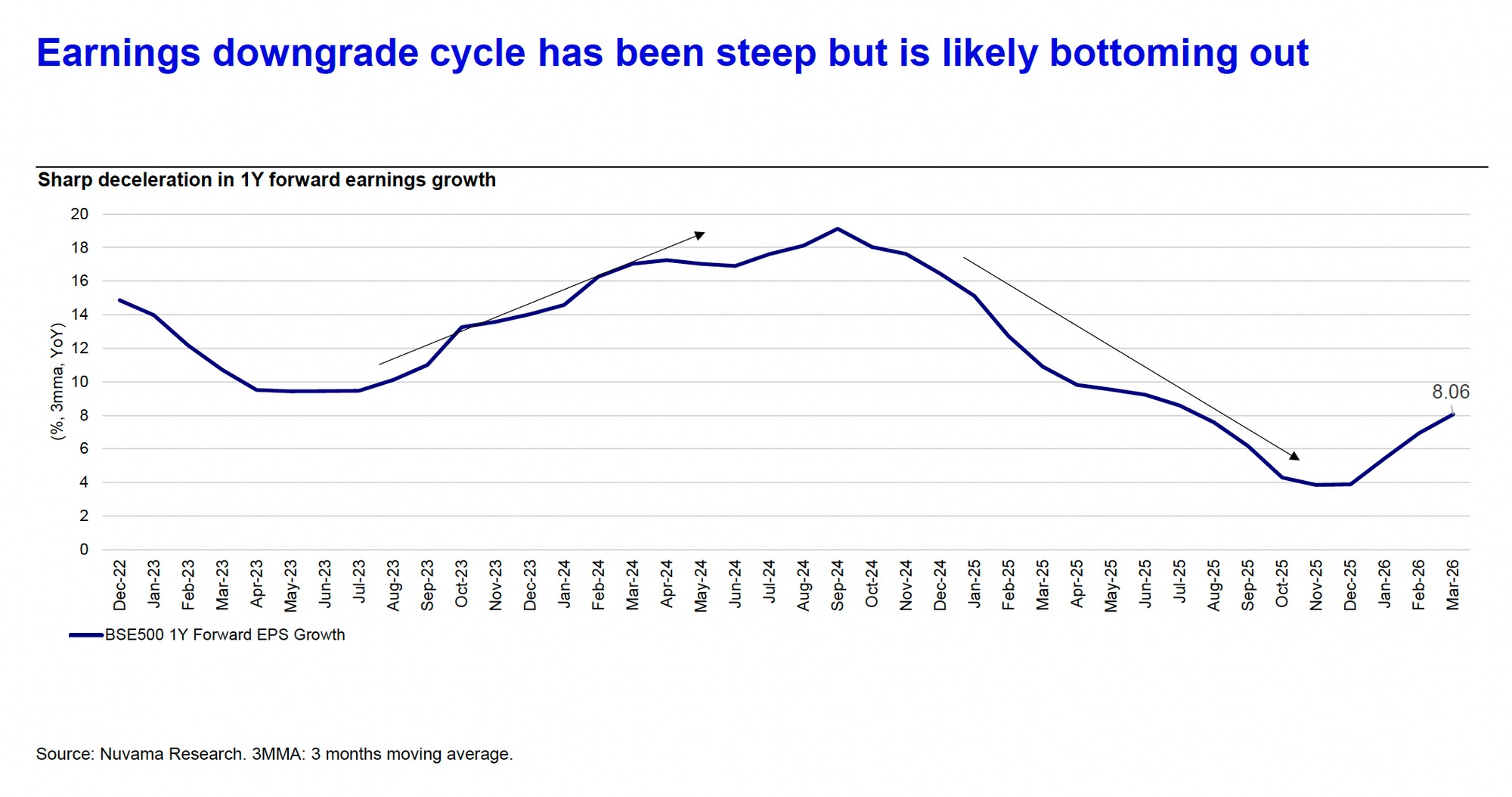

India’s earnings trajectory is beginning to look meaningfully stronger.

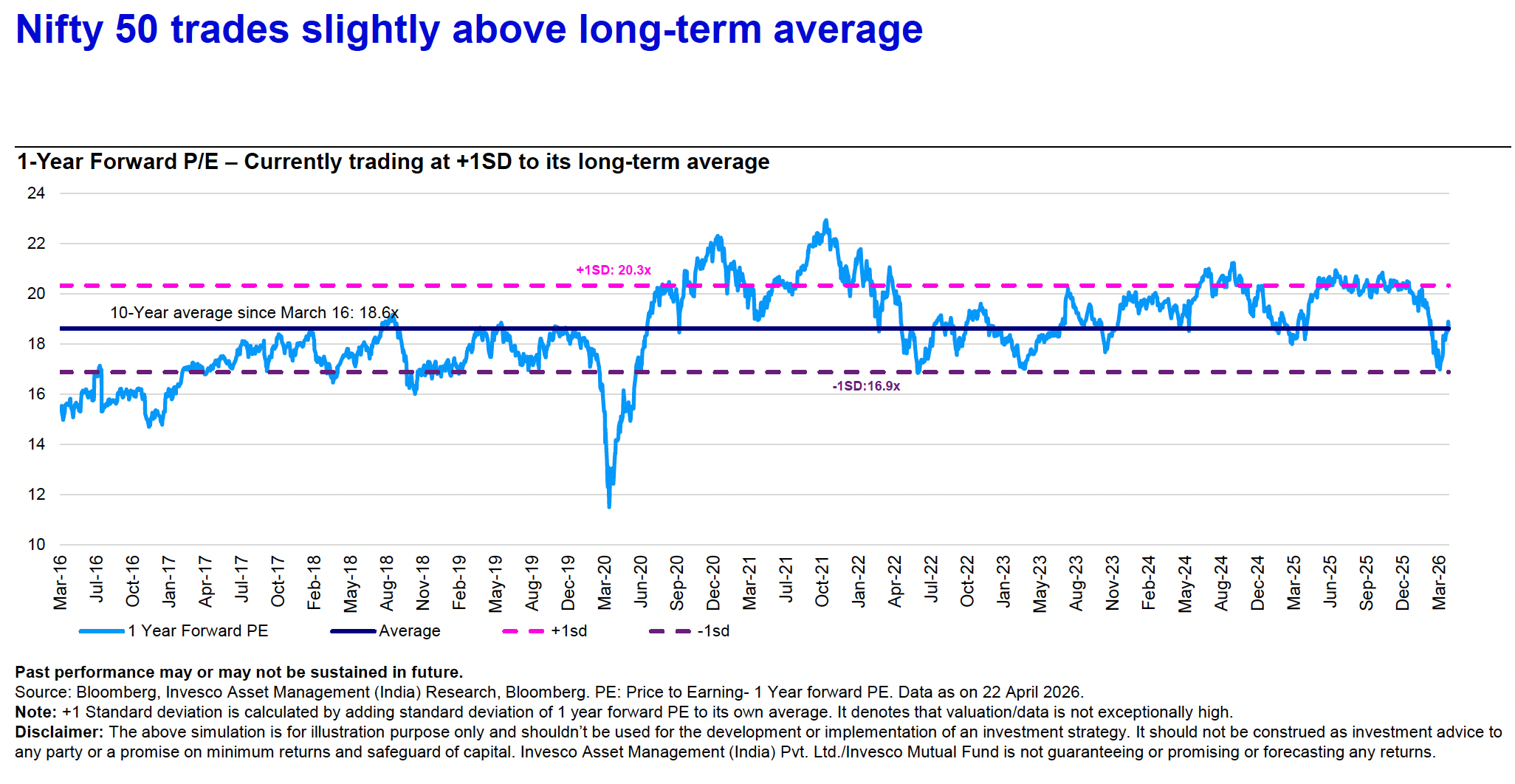

At present, the Nifty trades at roughly 20x forward earnings. While valuations are not extremely cheap, they appear reasonable when viewed alongside the improving earnings outlook.

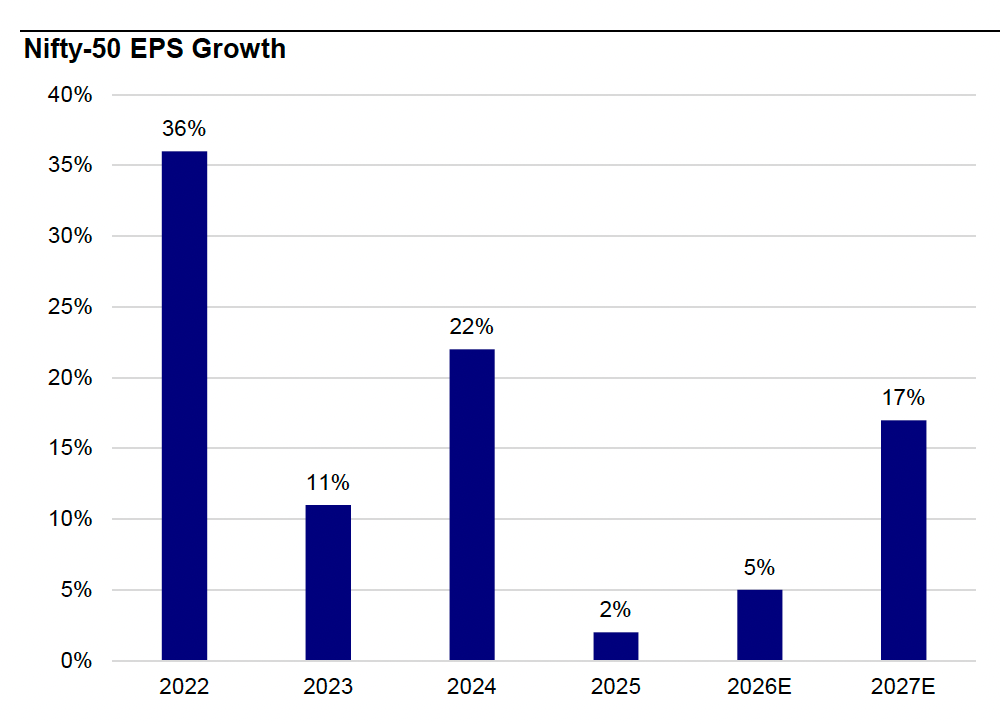

Current consensus expectations suggest:

• ~11% earnings growth this year

• ~17% earnings growth next year

However, we believe the more important takeaway is that India could sustain EPS growth in the range of 14–16% over the next few years if the current trajectory continues.

And if earnings growth remains durable, markets may also witness selective P/E re-rating alongside EPS expansion.

Put together, this creates a constructive setup for Indian equities over the medium term.

That said, we remain conscious of the global macro risks.

India continues to face structural challenges from:

• A large crude oil and energy import bill

• Weak balance-of-payments dynamics

• Dependence on foreign capital flows

These factors may continue to keep pressure on the INR for some time. However, we also believe the currency has already depreciated more than what current fundamentals justify, making the INR modestly undervalued at present levels.

At the same time, the global AI-driven rally — especially in developed markets — has made several international equity markets significantly more expensive relative to India.

That relative valuation gap matters.

As a result, we believe investors should gradually tilt portfolios more aggressively toward India over the coming years.

A reasonable allocation framework could be:

• Indian Equities: 70–80%

• Global Equities: 10–20%

• Gold: 5–10%

• Debt: Maintain strategic allocation

So what should investors do now?

If you have been sitting on large liquid balances waiting for clarity, this may be the time to start deploying capital gradually into Indian equities over the next 3–6 months.

We believe the current geopolitical uncertainty and ceasefire-related concerns are likely to prove more emotional than structural. If crude supply conditions improve over the coming quarters, oil prices could soften — reducing one of India’s biggest macro pressures.

Secondly, if you have recently received:

• Salary increments

• Promotions

• Bonus payouts

• Business surplus cash flows

…this may be the right time to substantially increase SIP allocations, even if it comes at the cost of moderating discretionary consumption temporarily.

The next few years could potentially become a meaningful wealth-creation cycle for Indian equities if earnings continue to compound at the current pace.

This is not be the phase to remain underinvested in India.